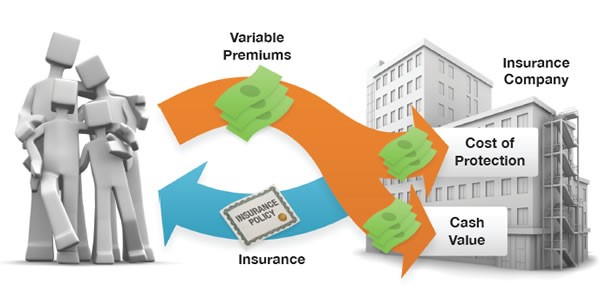

Universal life insurance is permanent life insurance — that is, it remains in force for your whole life. But universal life insurance has an important difference from other types of permanent insurance: it provides a flexible premium.

That means the policyholder decides how much to put in above a set minimum. By extension, the policyholder also determines the face amount of the policy.

Universal life insurance policies accumulate cash value — cash value that grows tax deferred. Guarantees are based on the claims-paying ability of the issuing company.

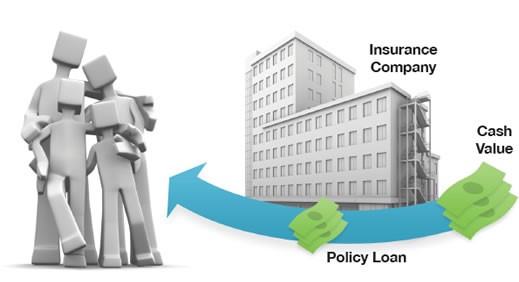

Universal life insurance policies normally let policyholders borrow a portion of their policy’s cash value under fairly favorable terms. And interest payments on policy loans go directly back into the policy’s cash value.*

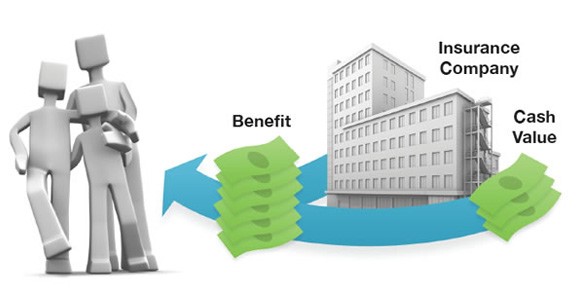

When the policyholder dies, his or her beneficiaries receive the benefit from the policy. Depending on how the policy is structured, benefits may or may not be taxable.

*Universal life insurance has certain features that make the policy suitable for some individuals. Whether universal life insurance is appropriate for you will depend on your goals, needs, and circumstances.

Accessing the cash value in your insurance policy through borrowing — or partial surrenders — has the potential to reduce the policy’s cash value and benefit. Accessing the cash value may also increase the chance that the policy will lapse and may result in a tax liability if the policy terminates before your death.

Universal life insurance can be structured so that the cash value that accumulates will eventually cover the premiums. However, additional out-of-pocket payments may be required if the policy’s dividend decreases or if investment returns underperform.

Several factors will affect the cost and availability of life insurance, including age, health, and the type and amount of insurance purchased. Life insurance policies have expenses, including mortality and other charges. If a policy is surrendered prematurely, the policyholder also may pay surrender charges and have income tax implications. You should consider determining whether you are insurable before implementing a strategy involving life insurance. Any guarantees associated with a policy are dependent on the ability of the issuing insurance company to continue making claim payments.

Withdrawals of earnings are fully taxable at ordinary income tax rates. If you are under age 59½ when you make the withdrawal, you may be subject to surrender charges and assessed a 10% federal income tax penalty. Also, withdrawals will reduce the benefits and value of the contract. Life insurance is not FDIC insured. It is not insured by any federal government agency or bank or savings association.

Generally, loans taken from a policy will be free of current income taxes, provided certain conditions are met, such as the policy does not lapse or mature. Keep in mind that loans and withdrawals reduce the policy’s cash value and death benefit. Loans also increase the possibility that the policy may lapse. If the policy lapses, matures, or is surrendered, the loan balance will be considered a distribution and will be taxable.

The Wealth Guardians are here to collaboratively help you determine if universal life insurance is appropriate for you. Click here to schedule a no-cost, no-obligation second opinion of your current plan. Or, give us a call at our Charlotte office at (704) 248-8549, or our Clemmons office at (336) 391-3409.

SOURCES:

- Original article by FMG Suite, 2020

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}